To achieve financial success, knowledge is key.

Yet many Americans lack financial literacy. That can impact everything from the amount of money saved to debt owed.

The situation is dire for more than a few. More than half of Americans can’t cover a $1,000 emergency expense with savings, a January survey from Bankrate found. Meanwhile, about 20% of employees run out of money before their next paycheck, according to Salary Finance. That’s up from 15% last year.

Meanwhile, U.S. adults correctly answered only 50% of the questions on the TIAA Institute-GFLEC Personal Finance Index in 2021, a noted measure of financial literacy. That’s 2 percentage points lower than the previous year.

“Financial literacy can help Americans feel confident about the decisions they make on a daily basis,” said NFL linebacker Brandon Copeland, who teaches a personal finance class at his alma mater, University of Pennsylvania.

“To expect success in anything I do, I must first understand the rules and guidelines of that game,” he added. “The same applies to understanding money and how it operates.”

Building good habits

These days, Americans are still grappling with the fallout from the Covid-19 pandemic and ensuing inflation, which is costing the average U.S. household an additional $296 per month, a Moody’s Analytics analysis found.

Yet there is always going to be something that may disrupt your life, said Nan Morrison, president and CEO of the Council for Economic Education.

“There are a lot of things that may impact your income or the world around us, but making a decision in the moment isn’t actually going to be that helpful,” she said.

“Having built the good habits that you need early in life…. will help to get through all those changes.”

Those behaviors include understanding where you stand financially, building a budget and saving for emergencies.

Saving and investing

Knowledge is also power when it comes to investing. While trading meme stocks and cryptocurrency has become popular, it’s important to remember that saving for the long-term is vital to your financial health, said certified financial planner Cathy Curtis, founder and CEO of Curtis Financial Planning in Oakland, California.

It was something she recently counseled her new hairdresser on, after he confided his anxiety around money and concern about providing financial stability for his family. The stylist, in his mid-40s, was invested in a fintech company stock and in crypto through a popular trading app, but had no retirement savings or life insurance.

“If my hairstylist knew the basics about Roth [individual retirement accounts], for example, starting many years ago, he would be so far ahead,” Curtis said.

“Without basic financial education about the power of compounding interest, what types of savings accounts and retirement accounts are available, and how important it is to start saving early, the financial future of many Americans is grim.”

Helping relationships

Couples may have different thoughts about money. When there is mismanagement of finances or a difference of opinion about how to use money, that can create conflicts.

“Many couples struggle to talk about money and if there is a lack of financial literacy in the couple, there could be many financial missteps,” said licensed marriage and family therapist Dr. George James, chief innovation officer and senior staff therapist at the non-profit Council for Relationships.

“Having a greater understanding of financial literacy can help relationships to build a future and be on the same page,” he added. “It can also reduce the amount of conflict.”

Personal finance in schools

Advocates believe its important to start learning good financial habits at a young age, and there’s no better place than in school.

Twenty-five states require high-school students to take personal finance coursework, either in a standalone class or integrated into another course, according to the Council for Economic Education. Last week, Florida became the latest to sign a bill into law mandating a course for graduation.

In addition, there are 46 personal finance bills currently pending in 21 states, according to Next Gen Personal Finance’s bill tracker.

The impact of that education can be seen in several studies, advocates argue. It has been shown to reduce the likelihood of using payday loans among young adults and is positively correlated with asset accumulation by age 25.

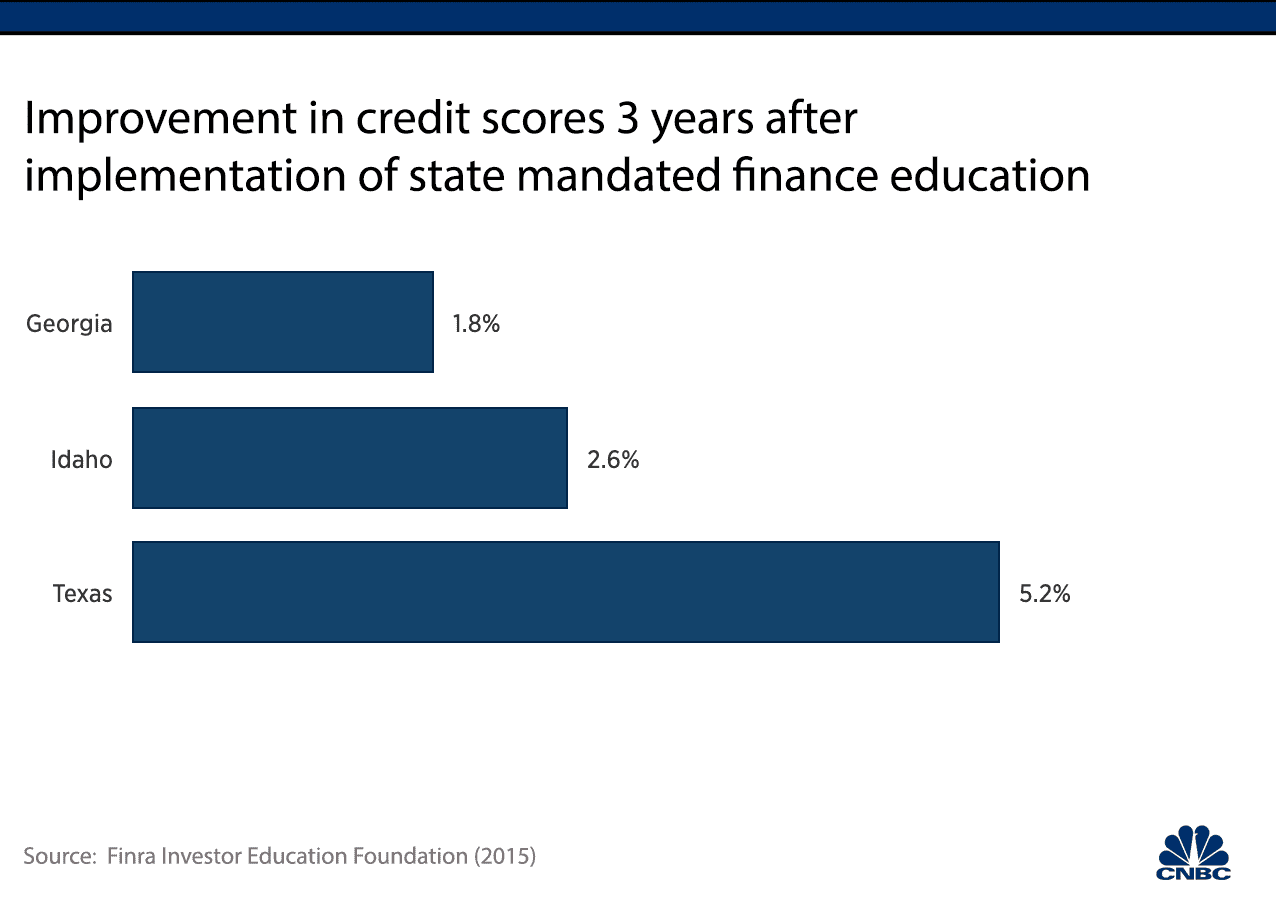

Another study that compared three states that mandated personal finance coursework to three states that didn’t found that credit outcomes improved in the mandate states. Three years after education was implemented in Georgia, Idaho and Texas, all three states saw a reduction in severe delinquency rates and credit scores rise.

“Schools are the great equalizer,” said Yanely Espinal, director of educational outreach at Next Gen Personal Finance.

“This is the opportunity for us to create access for all students regardless of their zip code, regardless of their parents’ knowledge level or income level, regardless of whether their families know this information or not.”

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.